Award-winning PDF software

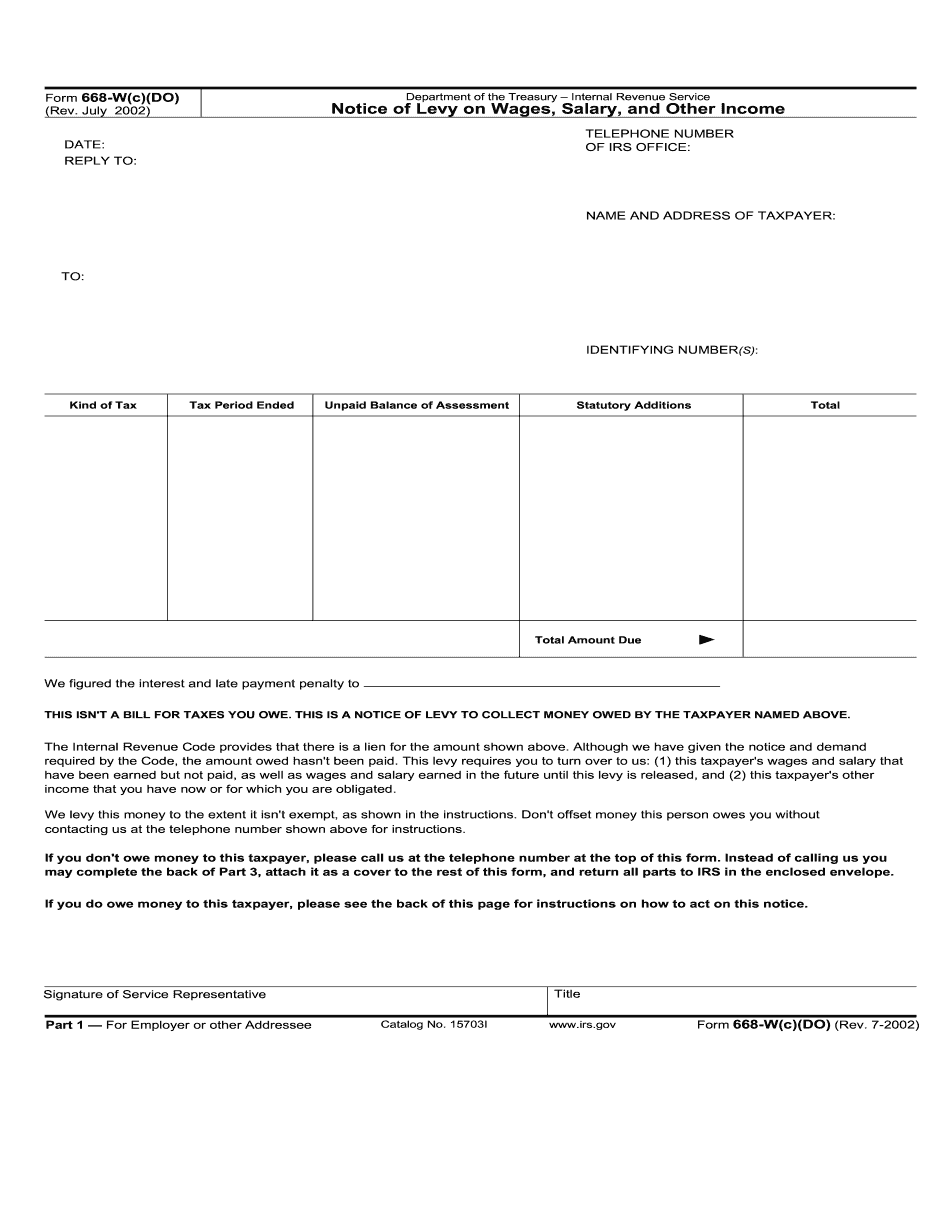

The Sample 668 W (c) is used by the Internal Revenue Service to inform a taxpayer and the employer about a levy against wages. In cases like this, the owner needs to turn over non-exempt one while the employee has to report on dependents. In order to release a levy, which is usually 90% of the wages, the will require the taxpayer to submit more information and complete Form 433 A and 433 F. The Service may give a release if the payer proves that it causes serious economic hardships for them.

Form 668 W (c) (DO): Who Sends it to Who?

The template is mailed by the Internal Revenue Service to an organization after the tax period when every employee has already claimed an income tax return. The employer is usually given one calendar period before exempting wages from employees. He or she is asked to encourage the staff to contact the Service to make sure that it’s not a mistake. In case it’s not a mistake, the employee can either discuss a release or figure out tax payments with the .

Where Should Form 668 W (c) (DO) Be Sent?

Usually, Internal Revenue Service levies are delivered by mail to the employer. The date when the levy was received is considered to be the date it begins. If it covers bank accounts, the taxpayer has 21 days to contact the and arrange a form of payment before the bank pays it.