PDF editing your way

Complete or edit your irs levy bank account anytime and from any device using our web, desktop, and mobile apps. Create custom documents by adding smart fillable fields.

Native cloud integration

Work smarter and export form 668 w directly to your preferred cloud. Get everything you need to store, synchronize and share safely with the recipients.

All-in-one PDF converter

Convert and save your form 668 w 2021 as PDF (.pdf), presentation (.pptx), image (.jpeg), spreadsheet (.xlsx) or document (.docx). Transform it to the fillable template for one-click reusing.

Faster real-time collaboration

Invite your teammates to work with you in a single secure workspace. Manage complex workflows and remove blockers to collaborate more efficiently.

Well-organized document storage

Generate as many documents and template folders as you need. Add custom tags to your files and records for faster organization and easier access.

Strengthen security and compliance

Add an extra layer of protection to your irs wage levy by requiring a signer to enter a password or authenticate their identity via text messages or phone calls.

Company logo & branding

Brand your communication and make your emails recognizable by adding your company’s logo. Generate error-free forms that create a more professional feel for your business.

Multiple export options

Share your files securely by selecting the method of your choice: send by email, SMS, fax, USPS, or create a link to a fillable form. Set up notifications and reminders.

Customizable eSignature workflows

Build and scale eSignature workflows with clicks, not code. Benefit from intuitive experience with role-based signing orders, built-in payments, and detailed audit trail.

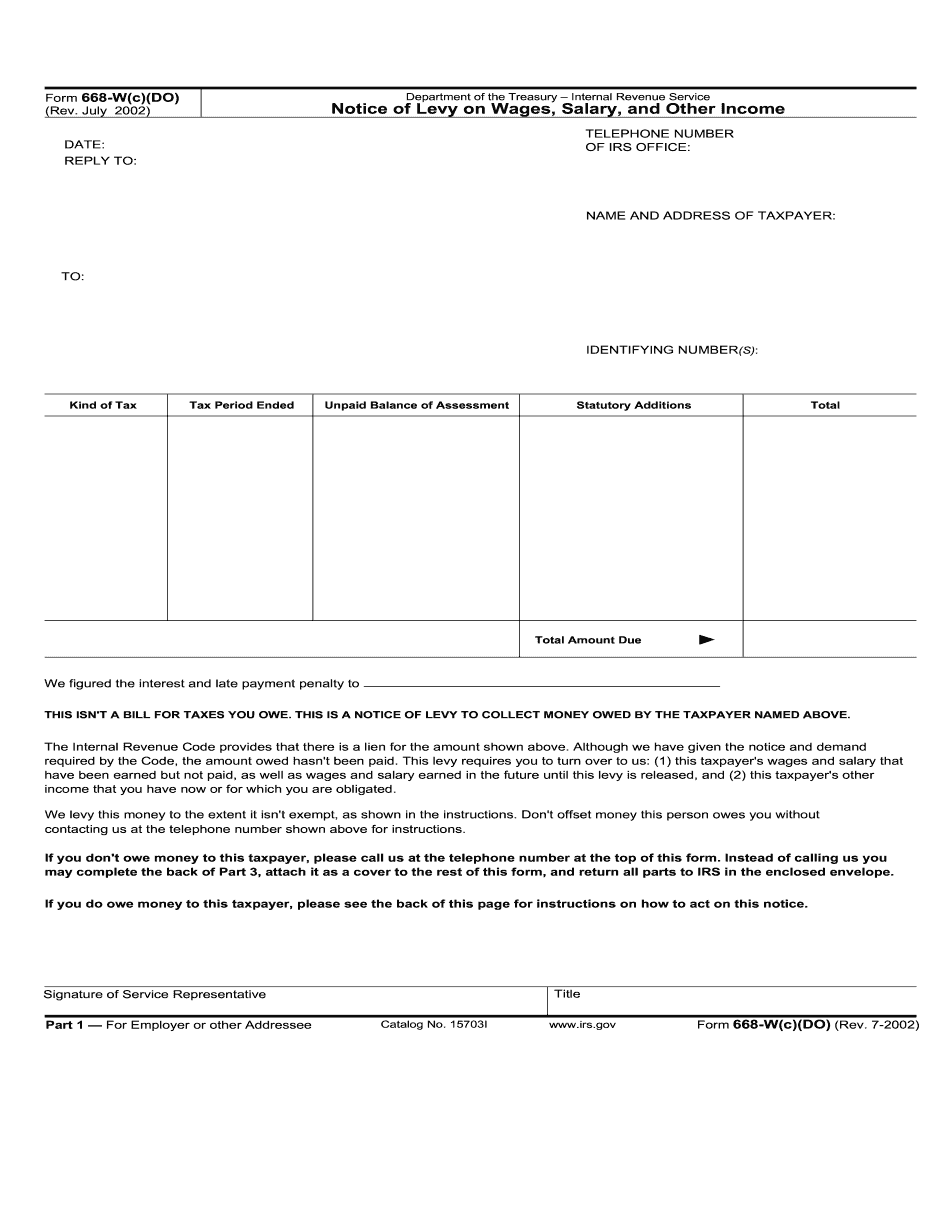

What you should know about Tax Levy on Bank Account

- Form 668-W requires the turnover of wages, salary, and other income earned by the taxpayer.

- The form is used to collect money owed by the taxpayer through a notice of levy.

- Exempt amounts from the levy must be claimed by completing the Statement of Exemptions and Filing Status.

Award-winning PDF software

How to prepare Tax Levy on Bank Account

About Form 668-W(c)(DO)

Form 668-W(c)(DO) is a notice of levy on wages, salary, and other income. This form is used by the Internal Revenue Service (IRS) to initiate a wage garnishment to collect outstanding tax debts. It is typically sent to an employer to inform them that they are required by law to withhold a certain percentage of an employees pay and send it directly to the IRS until the tax debt is satisfied. This form is needed by the IRS to collect unpaid taxes from individuals who have failed to pay their tax liabilities. It is also necessary for employers who receive this notice to comply with the wage garnishment order and withhold the specified amount from their employees paychecks until the debt is paid in full. The purpose of this form is to ensure that taxpayers fulfill their obligation to pay taxes owed and to protect the governments interest in collecting unpaid taxes.